Click on the companies below for Graham Evaluation:

Aalberts Industries 2023

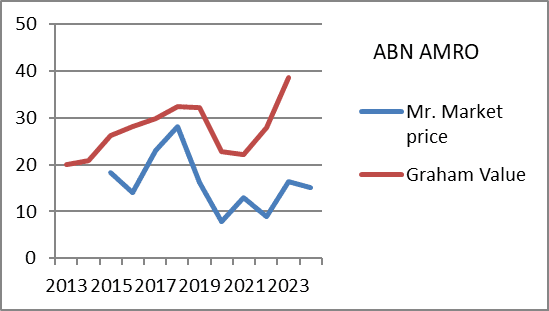

ABN AMRO 2023

Ahold Delhaize Koninklijke 2022

Accsys Technologies 2022

Aalberts Industries 2023

ABN AMRO 2023

Ahold Delhaize Koninklijke 2022

Accsys Technologies 2022

Adux: French holding company, no English or Dutch info? https://www.adux.com/en/investors/

HAL Trust 2022 a buy at EUR 108?

Heijmans 2022

Heineken 2022

Holland Colours 2022

Hydratec 2022 taken private in 2024 for EUR 142

IEX Group 2022

IMCD 2022

ING Bank 2022

Adyen 2022 Part Deux

Aedifica 2022

Aegon 2022 too difficult pile

AFC AJAX 2022

Air France-KLM 2022

Akzo Nobel 2022

Alfen 2023

Alumexx 2022 (voorheen Phelix, Inverko, Newconomy)

Aedifica 2022

Aegon 2022 too difficult pile

AFC AJAX 2022

Air France-KLM 2022

Akzo Nobel 2022

Alfen 2023

Alumexx 2022 (voorheen Phelix, Inverko, Newconomy)

Alumunda (voorheen Novisource) 2022

AMG Advanced Metallurgical Group NV LITHIUM 2022

Amsterdam Commodities ACOMO 2022

AMG Advanced Metallurgical Group NV LITHIUM 2022

Amsterdam Commodities ACOMO 2022

Azerion 2022

BAM Koninklijke Groep 2022

Basic Fit 2022

BE Semiconductor AEX:BESI 2022

B&S Group 2022

Berkshire Hathway 2022

BAM Koninklijke Groep 2022

Basic Fit 2022

BE Semiconductor AEX:BESI 2022

B&S Group 2022

Berkshire Hathway 2022

Bever Holding 2022

Boussard & Gavaudan Holding Ltd. An expensive hedge fund.

Boussard & Gavaudan Holding Ltd. An expensive hedge fund.

ENTP Energy Transition Partners SPAC Jan 21st 2024 deadline

Eurocastle 2022

Eurocommercial Properties 2022

Euronext 2022

Eurocastle 2022

Eurocommercial Properties 2022

Euronext 2022

HAL Trust 2022 a buy at EUR 108?

Heijmans 2022

Heineken 2022

Holland Colours 2022

Hydratec 2022 taken private in 2024 for EUR 142

IEX Group 2022

IMCD 2022

ING Bank 2022

Just Eat Takeaway.com 2022

Kendrion 2022

KPN 2022

K. Porceleyne Fles Koninklijke 2022

K. VOPAK 2022

Lavide Holding 2022 Fair Finance Firm?

MAJOREL GROUP LUX

Kendrion 2022

KPN 2022

K. Porceleyne Fles Koninklijke 2022

K. VOPAK 2022

Lavide Holding 2022 Fair Finance Firm?

MAJOREL GROUP LUX

Marel 2022 ?

Nedap 2022

MKB Nedsense 2022

Morefield Group 2022

New Sources Energy 2022

Nedap 2022

MKB Nedsense 2022

Morefield Group 2022

New Sources Energy 2022

PB Holding Bovemij 2022 (voorheen Stern)

Pershing Square dec 2023

Pharming 2022

Philips 2022

PostNL 2022

Pershing Square dec 2023

Pharming 2022

Philips 2022

PostNL 2022

UMG

Unibail Rodamco 2022 still a buy?

Unilever 2022

Value8 2023

Van Lanschot Kempen 2023

Vastned Retail 2023

Volta Finance 2023 10% dividend

WDP 2023

Wereldhave 2023

Wolters Kluwer 2023

R.I.P.

Unibail Rodamco 2022 still a buy?

Unilever 2022

Value8 2023

Van Lanschot Kempen 2023

Vastned Retail 2023

Volta Finance 2023 10% dividend

WDP 2023

Wereldhave 2023

Wolters Kluwer 2023

R.I.P.

Accell Group 2020 taken private at EUR 58 in 2022, great price for shareholders.

Altice 2020 end of December 2020

Batenburg Techniek: Taken off the stock exchange for 46 Euros by van Puijenbroek family. Good price for investors: http://sinaas.blogspot.com/2018/08/batenburg-techniek-graham-valuation.html

BinckBank 2019 Saxobank

BinckBank 2019 Saxobank

Beter Bed Holding 2021 bought for EUR 5,74 per share

Boskalis Westminster Koninklijke 2021 bought in 2022 by HAL Trust for EUR 33 per share

Brill, Koninklijke 2022 private after more than 100 years 2023.

Curetis 2019 traded May 2020 for EUR 0,29

DPA Groep N.V. 2022

Esperite: 2018 Stem Cell Bank losing money, selling shares. Price recently fell from 3 to 0,25

oktober 2019 falliet, koers: 0,046 geen handel.

Esperite: 2018 Stem Cell Bank losing money, selling shares. Price recently fell from 3 to 0,25

oktober 2019 falliet, koers: 0,046 geen handel.

FNG 2019 Failliet 2022 https://fngnv.com/17-02-2022-fng-nv-vraagt-faillissement-aan/

Gemalto Thales offer 2018

Gemalto Thales offer 2018

GeoJunxion formerly AND 2023 EUR 1,1 distribution

Hunter Douglas 2021 bought for EUR 175

Kardan 2019 June 2020: https://www.iex.nl/Nieuws/ANP-240620-111/Kardan-geeft-beursnotering-in-Amsterdam-op.aspx

Klepierre cheap at €20? 2019 French

K. VolkerWessels 2019 taken private (again) in 2020

Lucas Bols 2022 2023 Nolet buyout EUR 18 at Graham Value

Oranjewoud 2018 EUR 6 2022 https://www.tubantia.nl/enschede/sanderink-is-gesteggel-met-toezichthouder-afm-beu-en-haalt-oranjewoud-van-de-beurs~a1cadfeb/

Thoughts on share prices: Peter Lynch and Nick Kraakman https://www.valuespreadsheet.com/blog/dangerous-sayings-about-stock-prices